PonyWang/E+ via Getty Images

Corsair Gaming (NASDAQ:CRSR), the gaming and streaming component and peripheral manufacturer, has reported several its Q4/2023 and Q1/2024 results after my previous analysis, and given the company’s 2024 financial guidance.

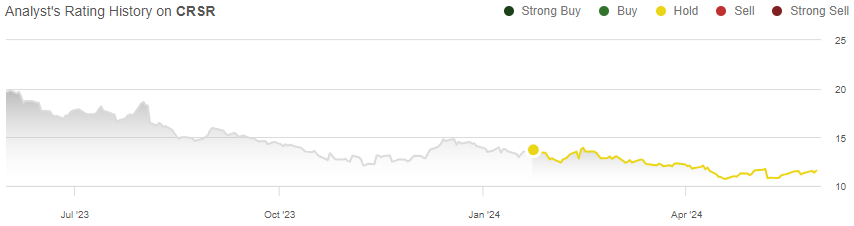

In my previous article, published on the 23rd of January with the title “Corsair’s Earnings Growth Is Priced In”, I estimated Corsair to continue growing its earnings well after a significant post-Covid revenue slump and a tough macroeconomic backdrop. I initiated the stock at a hold rating as the valuation seemed to already price in quite a large amount of earnings growth from the future. Since, Corsair has started to report lagging growth sending the stock downwards – from the publishing of my previous article, the stock has returned a negative -18% compared to an S&P 500 return of 7% in the same period.

My Rating History on CRSR (Seeking Alpha)

Soft End to 2023 & Weak Q1 Component Sales

After my previous article, Corsair posted its Q4 earnings on the 13th of February showing revenues of $417.3 million, up 4.7% year-over-year. The adjusted EPS came in at $0.22, up by 10% year-over-year. Both revenues and the EPS missed analysts’ estimates, although only by quite a small margin. While the revenue growth in Q4 was significantly slower than in the two previous quarters, it still showed healthy growth.

The more recently reported Q1 results showed a much worse performance, posted on the 7th of May. Revenues ended up -4.7% lower year-over-year at $337.3 million, and the adjusted EPS ended up at $0.09, down by $0.02 year-over-year.

The Q1 results missed estimates by a wide margin – revenues missed by $25.5 million as analysts expected positive growth, and the normalized EPS missed estimates by $0.05, both dragged by a weak stage in the GPU sales cycle according to Corsair’s earnings presentation. As a result, the Gaming Components and Systems segment pulled net revenues downwards despite very healthy growth of 20.3% in the Gamer and Creator Peripheral segment. The stock fell by -8% the following day of the post-market quarterly report.

I believe that the weak component sales can potentially be excused, but should be looked at critically – for example, Nvidia (NVDA) reported a year-over-year growth of 18% in gaming segment revenues in Q1, with the company being the most significant manufacturer of GPUs, making Corsair’s notation of a weak GPU cycle intriguing. On the other hand, AMD (AMD) did report a dramatic -48% year-over-year drop min gaming revenues in Q1, relating the decline partly to poor GPU sales.

The peripheral segment’s growth of 20.3% was incredibly strong, though. Publicly traded competitors in the segment seem to have achieved less growth. For example, Turtle Beach (HEAR) achieved growth of 8.6% in the quarter, and Logitech International (LOGI) only achieved 5.4% in revenue growth.

Corsair’s 2024 Guidance Expects Gradual Improvements

Corsair announced the company’s 2024 financial outlook with the Q4/2023 report. The company expects revenues of $1.45 billion to $1.60 billion, with the middle point representing a growth of 4.5% year-over-year. The adjusted operating income is expected at $92 million to $112 million, up from $85.4 million in 2023.

With Q1 showing a revenue decline, the guidance anticipates sequential improvements into greater growth – Corsair should return to good growth in H2 if the guidance holds water. Corsair reiterated the guidance in Q1 despite a weak quarter, as the company expects new product launches and expansion in the retail network. I believe that the revenue range can easily be reached if peripheral sales continue to carry the good growth momentum.

Future Growth Is Still Priced In

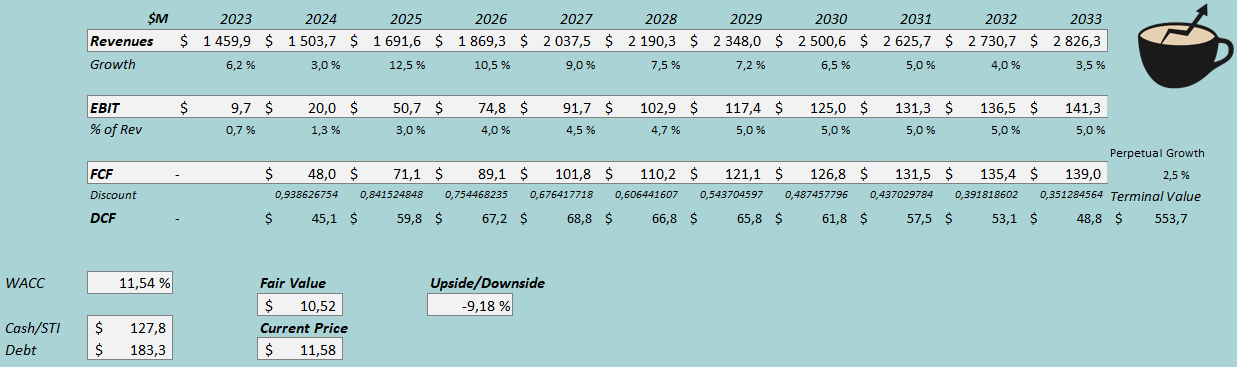

To evaluate the current valuation, I updated my DCF model. I now estimate weaker growth of only 3% in 2024 compared to 10% previously, but stronger growth afterwards as component sales seem to be pushed back. I still overall estimate a similar revenue performance with revenues ending at $2731 million in 2032 compared to a previous estimate of $2739 million. Afterwards, though, I have updated the perpetual growth estimate downwards from 3.0% into 2.5%.

As Corsair continues to post thin margins, I have adjusted margin expansion estimates downwards despite quite a good gross margin performance – I now estimate the GAAP EBIT margin to end up at 5.0% compared to a previous estimate of 6.0%.

With these updates, the DCF model estimates Corsair’s fair value at $10.52, around 9% below the stock price at the time of writing. The fair value is down by -14% from a previous estimate of $12.25. Despite a lower stock price, Corsair’s growth story still doesn’t look to pose upside unless long-term growth surprises the estimates very positively.

DCF Model (Author’s Calculation)

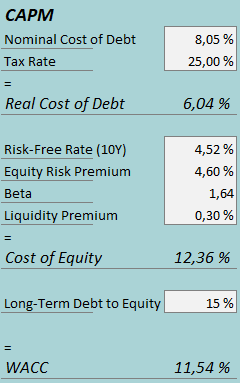

A weighted average cost of capital of 11.54% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Corsair had around $3.7 million in interest expenses. With the company’s current amount of interest-bearing debt, Corsair’s annualized interest rate comes up to 8.05%, up slightly from the previous interest rate estimate of 7.67%. The company has managed to pay off some of its debt, but as the equity value has decreased, my long-term debt-to-equity ratio remains at 15%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.52%. The equity risk premium of 4.60% is Professor Aswath Damodaran’s latest estimate for the United States, updated on the 5th of January. I keep the beta estimate the same at 1.64. Finally, I add a small liquidity premium of 0.3%, creating a cost of equity of 12.36% and a WACC of 11.54%. The WACC is up by 37 basis points from my previous estimate due to a higher interest rate and risk-free rate.

Takeaway

Corsair has posted weaker growth after my previous article. The company’s revenues turned into declines in Q1 as component sales drag financials, partly compensated by great peripheral momentum. The company still guides for 2024 revenue growth, implying a better back half to the year. While I believe that the growth story stands almost as strong, the valuation still doesn’t pose upside with the currently lower valuation. As such, I keep my rating on Corsair at hold.