djmilic/iStock via Getty Images

Investment Thesis

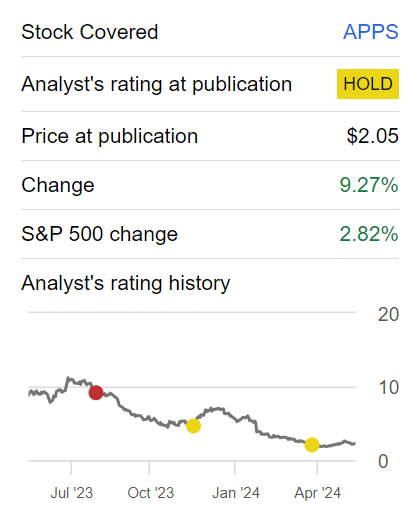

Digital Turbine’s (NASDAQ:APPS) prospects are less enticing than I previously believed. On the back of its fiscal Q4 2024 results, the stock fell 7% after hours. Indeed, as I look through these results, I’ve now downwards revised this stock from a hold to a sell.

There’s no point in overcomplicating this thesis. This business is a dead company walking and investors would do well to recognize this aspect, salvage their capital, and redeploy it elsewhere.

Crucially, this business’ debt has created a noose around it, making any attempt to reinvest in its operations prohibitive.

Rapid Recap

Last month I wrote an analysis titled Do Not Buy This Stock, where I said,

Even though the stock may have the occasional pop from quarter to quarter, in the medium and long-term, this business is uninvestable. In time, investors will look back to Digital Turbine’s $2.20 as a high price to aspire towards. Avoid this stock.

Author’s work on APPS

Since then, the stock picked up a bid, with my timing for writing that analysis been poor. Nonetheless, I remain resolute that this stock should be avoided, and as such, now rate the stock as a sell, rather than just a hold.

Digital Turbine’s Near-Term Prospects

Digital Turbine strives to make it easier for people to discover and use apps on their mobile devices. They partner with mobile carriers and phone makers to pre-install apps on new smartphones. Additionally, they offer a platform for app developers to promote their apps to more users. Their goal is to become a successful app distribution platform.

Moving on, during the earnings call, Digital Turbine’s management made the case that the company has laid a foundation for expansion through significant investments in strategic partnerships. Notably, the integration of new device capabilities through collaborations with global OEMs like Motorola and the introduction of Ignite on 70 million additional devices signal an interesting opportunity.

And yet, despite these promising prospects, Digital Turbine faces key headwinds too. One of the foremost issues is the sluggishness in US device sales. Postpaid upgrade rates in the US have been particularly low, with only 3% of users upgrading in the March quarter, implying a very slow upgrade cycle. This trend severely constrains the company’s ability to monetize through new device activations, which is a critical component of its revenue model. Additionally, the reduction in software updates on existing devices further diminishes monetization opportunities, compounding the challenge posed by stagnant device sales.

Another major challenge is Digital Turbine’s efforts to transition its revenue base to align with new regulatory environments, such as those influenced by the EU’s Digital Markets Act, which could introduce further operational complexities and delays.

Given this context, let’s now delve into its financials.

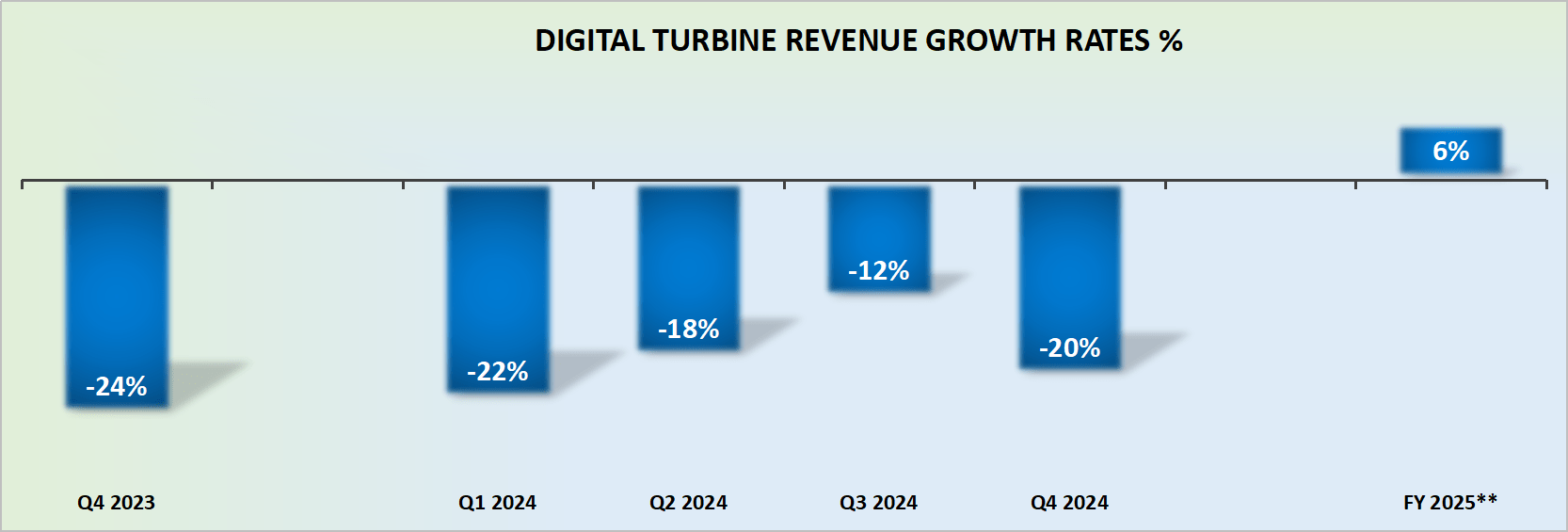

Fiscal 2025 Points to 6% Revenue Growth

APPS revenue growth rates

In my previous analysis, I said,

For a while, Digital Turbine had a better mousetrap. And was massively successful. For a while. But now looking ahead, I believe its task will be one of focusing and reshaping and stabilizing its operations, rather than finding another growth driver.

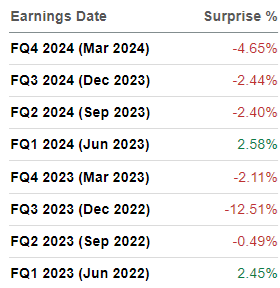

In an effort to echo my contention, consider the graphic that follows, where we see Digital Turbine’s revenue beats and misses.

SA Premium

As a whole, in the past 2 years, Digital Turbine mostly missed analysts’ estimates. This is not a promising foundation from whence to invest one’s hard-earned capital.

APPS Stock Valuation – 2x EBITDA

Digital Turbine holds very approximately $350 million of net debt. Think about this for a moment. This figure is higher than its market cap. While I recognize that investors reading this page are only taking on the equity part of the business, the fact that the equity is trading for less than debt should tell you everything you need to know about APPS. There’s no need to overcomplicate this thesis further.

That being said, if we did find ourselves with a proclivity towards overcomplicating what is rather straightforward, we’d question how will Digital Turbine navigate the next twelve months?

When all was said and done, Digital Turbine’s fiscal 2024 delivered approximately $5 million of free cash flow. Or put more starkly, out of the $92 million of EBITDA reported in fiscal 2024, the actual free cash flow was less than $10 million.

How will Digital Turbine make its creditors whole? This debt becomes due in April, two years from now.

Yes, the stock appears cheaply valued at 2x EBITDA. But this EBITDA has a poor free cash flow conversion ratio. And on top of that, the business is hardly growing. All in all, this stock is an easy sell. There are so many better opportunities for one to deploy one’s capital, with more favorable risk-reward profiles.

The Bottom Line

In conclusion, Digital Turbine’s financial health reveal significant yellow flags. The company holds approximately $350 million in net debt, exceeding its market cap, and its fiscal 2024 free cash flow was a mere $5 million from $92 million in EBITDA. This poor free cash flow conversion ratio, combined with stagnant revenue growth and consistent misses on analysts’ estimates, underscores a precarious financial situation.

Despite appearing cheap at 2x EBITDA, the lack of growth and heavy debt burden make this stock a clear sell.

Investors would be wise to seek more favorable opportunities elsewhere.