Editor’s note: Seeking Alpha is proud to welcome Florian Muller as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Armando Oliveira/iStock Editorial via Getty Images

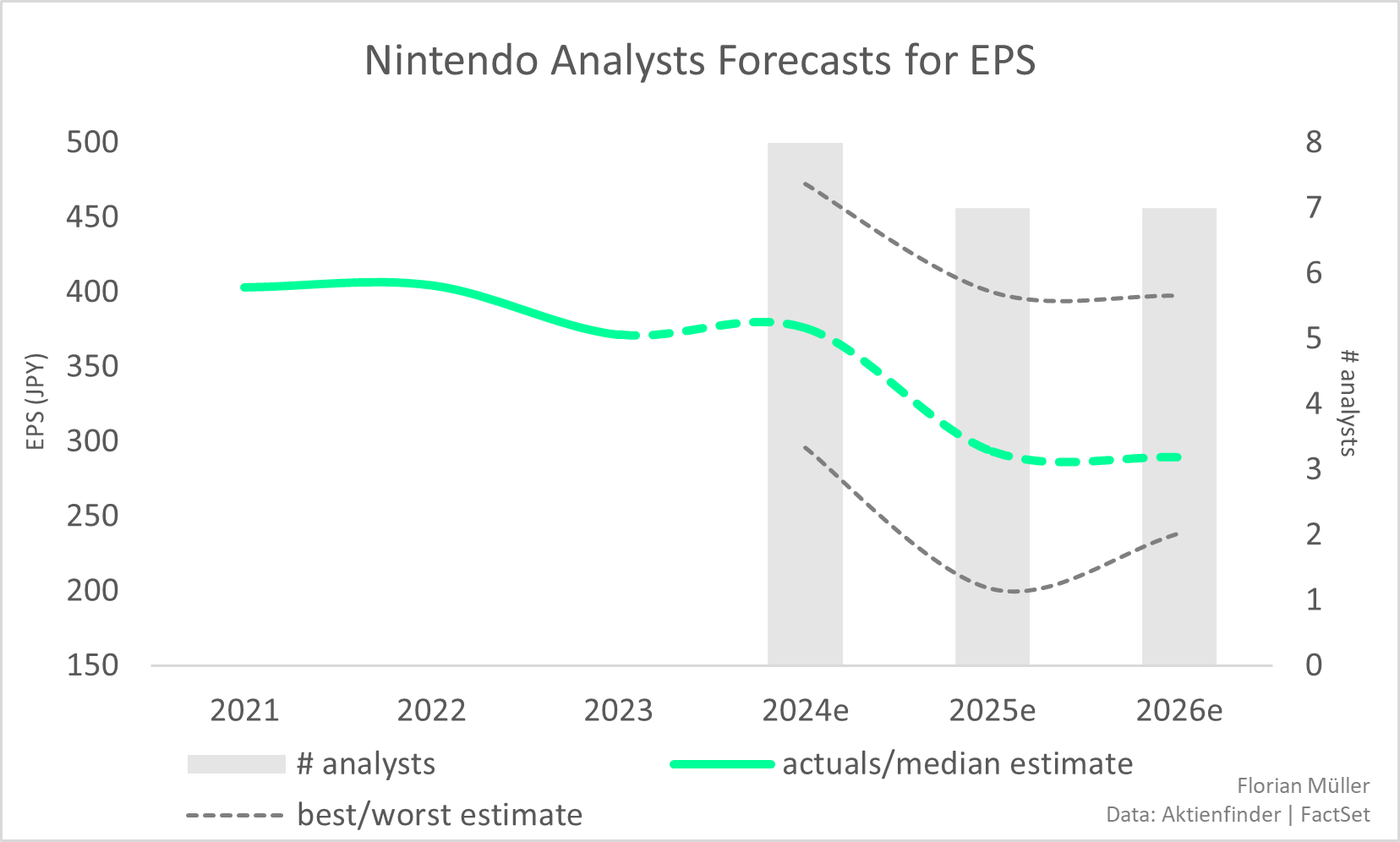

One might think that, at least in the short term, Nintendo (OTCPK:NTDOF) (OTCPK:NTDOY) is not a top pick purely based on earnings, given its anticipated business contraction according to the median analysts’ forecasts shown below. Some could claim that at best the company offers an appealing narrative for die-hard fans. As for myself, I’ve identified compelling reasons to remain loyal to my current position in the stock. I will explain these in the sections that follow.

Florian Müller | Data: Aktienfinder.net, FactSet

About half of Nintendo’s software sales are digital, which could potentially hold further margin opportunities in the long term, offsetting declining revenues. Arguments like these, among others, have been exhaustively stressed in other analyses and hold true for Nintendo. I, however, will base my analysis on four key pillars:

- How Nintendo leverages currency risks

- How Nintendo generates value from its cash surplus

- Nintendo’s product excellence and Intellectual Property strategy

- A discounted cash flow valuation

Navigating and Leveraging Currency Risks

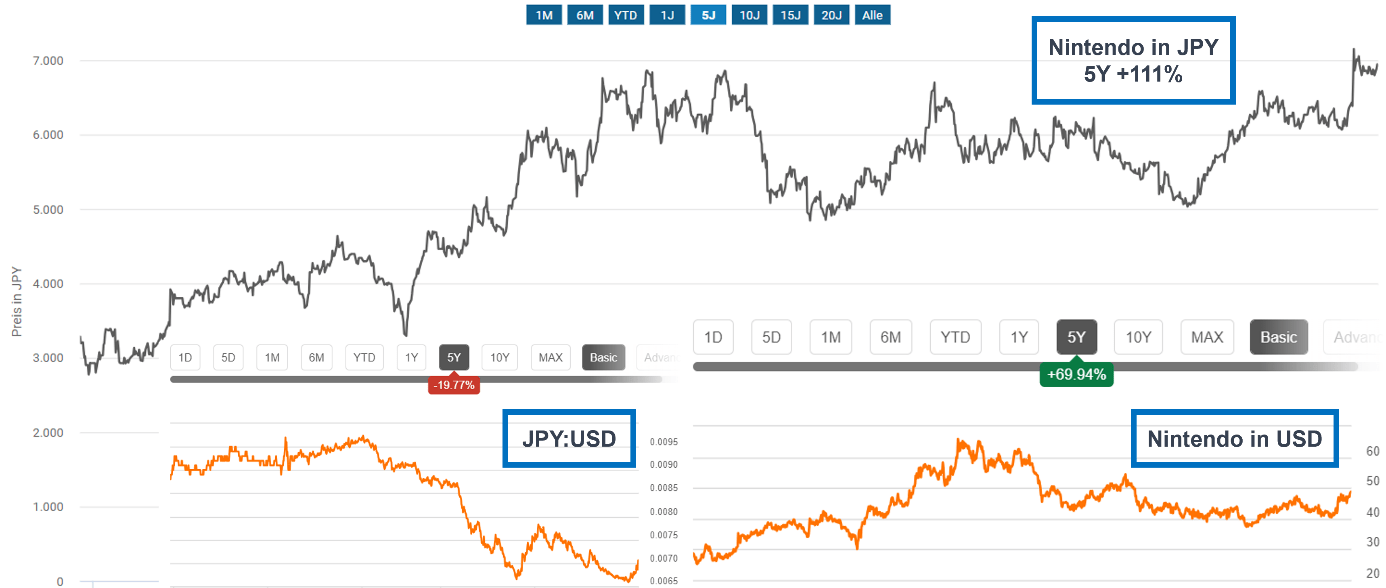

In the past five years, Nintendo’s stock, listed in Japanese Yen on the Tokyo Stock Exchange, has surged by more than 110%. During the same period, the Japanese Yen has depreciated by almost 20% against the US Dollar – or conversely, the US Dollar has appreciated by 25 percent against the Japanese Yen. Consequently, US investors, when evaluated in US Dollars, have gained approximately 70% in Nintendo’s stock over the last five years, as opposed to the perceived 110%. A significant portion of the gains has been mitigated by the weakening Yen. While this analysis doesn’t aim to extensively address macro issues such as currency fluctuations, this example vividly illustrates the currency risk associated with the Japanese Yen and thus, associated with Nintendo from the perspective of an investor outside Japan.

Aktienfinder.net, Seeking Alpha

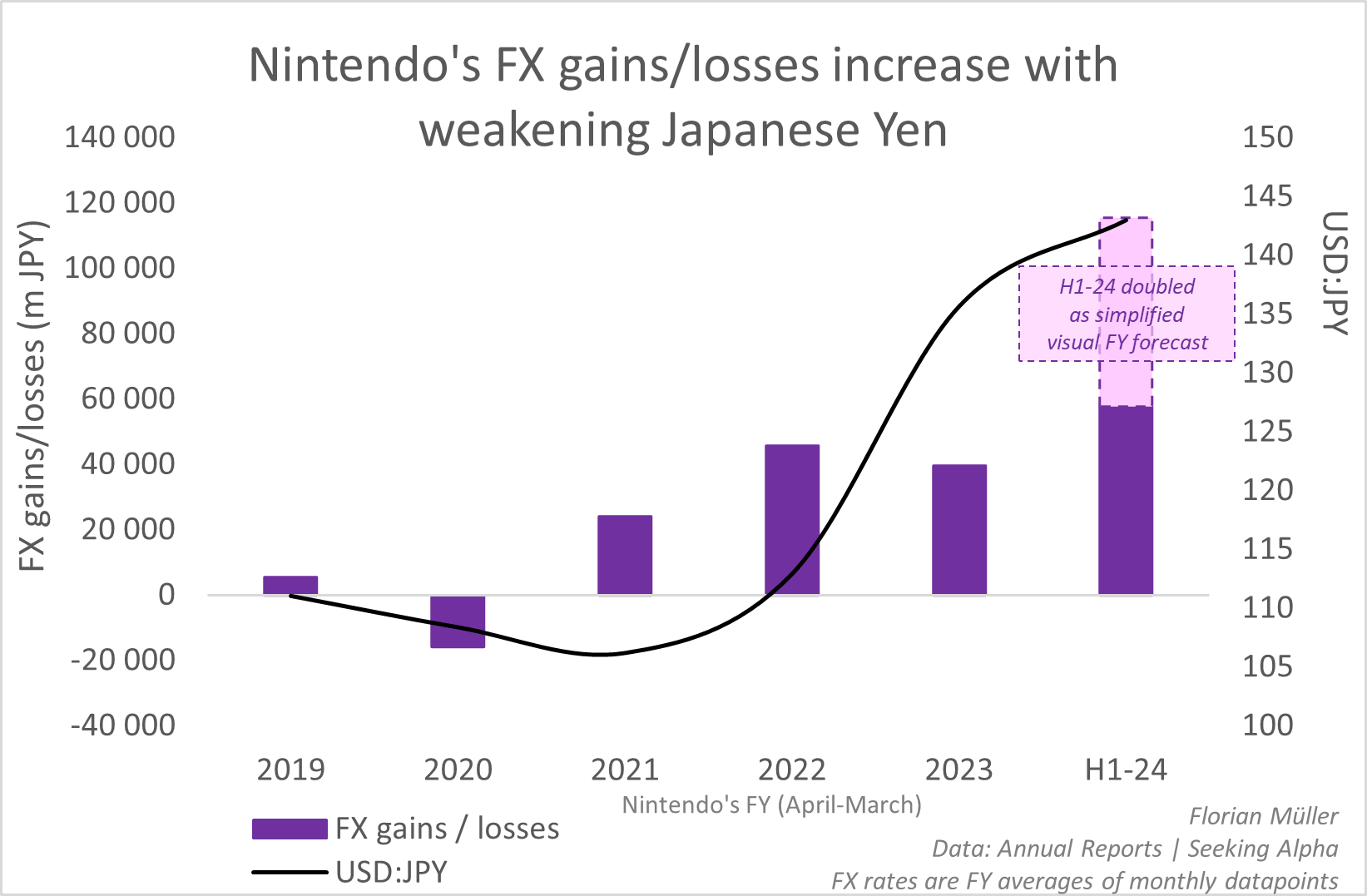

Nevertheless, the company strategically leveraged this vulnerability in both their operations and non-operating excess cash management. With only about 22% of its revenues recently generated in Japan, 23% in Europe, and 44% in “The Americas”, the appreciating USD played into the hands of the Japanese corporation when converted into yen. Compared to the previous first half-year, Nintendo’s net sales have increased by 21.2%, or 139.3 million yen, with 36.8 million yen, or 5.6%, attributed solely to the weak yen. Conversely, a re-strengthening yen could exert pressure on the sales side.

Additionally, cash-like assets held by Nintendo in foreign currencies resulted in non-operational foreign exchange gains. I have visually shown how Nintendo’s non-operating profits from investments in foreign currencies outside of JPY have markedly increased recently. As an example, I’ve displayed the strength of the US Dollar exchange rate alongside, which correlates with Nintendo’s gains from foreign currencies. This illustrates that the weak yen has played into Nintendo’s hand not just operationally, but also due to its high cash surpluses and their short-term investments abroad.

Florian Müller | Data: Annual Reports, Seeking Alpha

High Interest Rates? Yes, Please!

An investment in Nintendo seems to be a comfortable position in both high and low-interest rate environments. While many indebted companies are struggling with increasing interest expenses, Nintendo sits on a substantial cash (& equivalents) pile of more than 2 trillion yen or $14 billion. This, in turn, is being lucratively invested as I will illustrate in a second. While economic conditions in many places may be slowing due to the rising interest rate environment, Nintendo is able to generate returns on its high liquidity reserves, bolstering its financial strength. Thus, Nintendo is armed to the teeth, ready to strategically allocate its cash reserves when the time is right, especially during the next phase of a new console release or a potential shift in global monetary policies. Its robust liquidity position empowers Nintendo to finance future growth initiatives independently and react swiftly to market changes and intense competition.

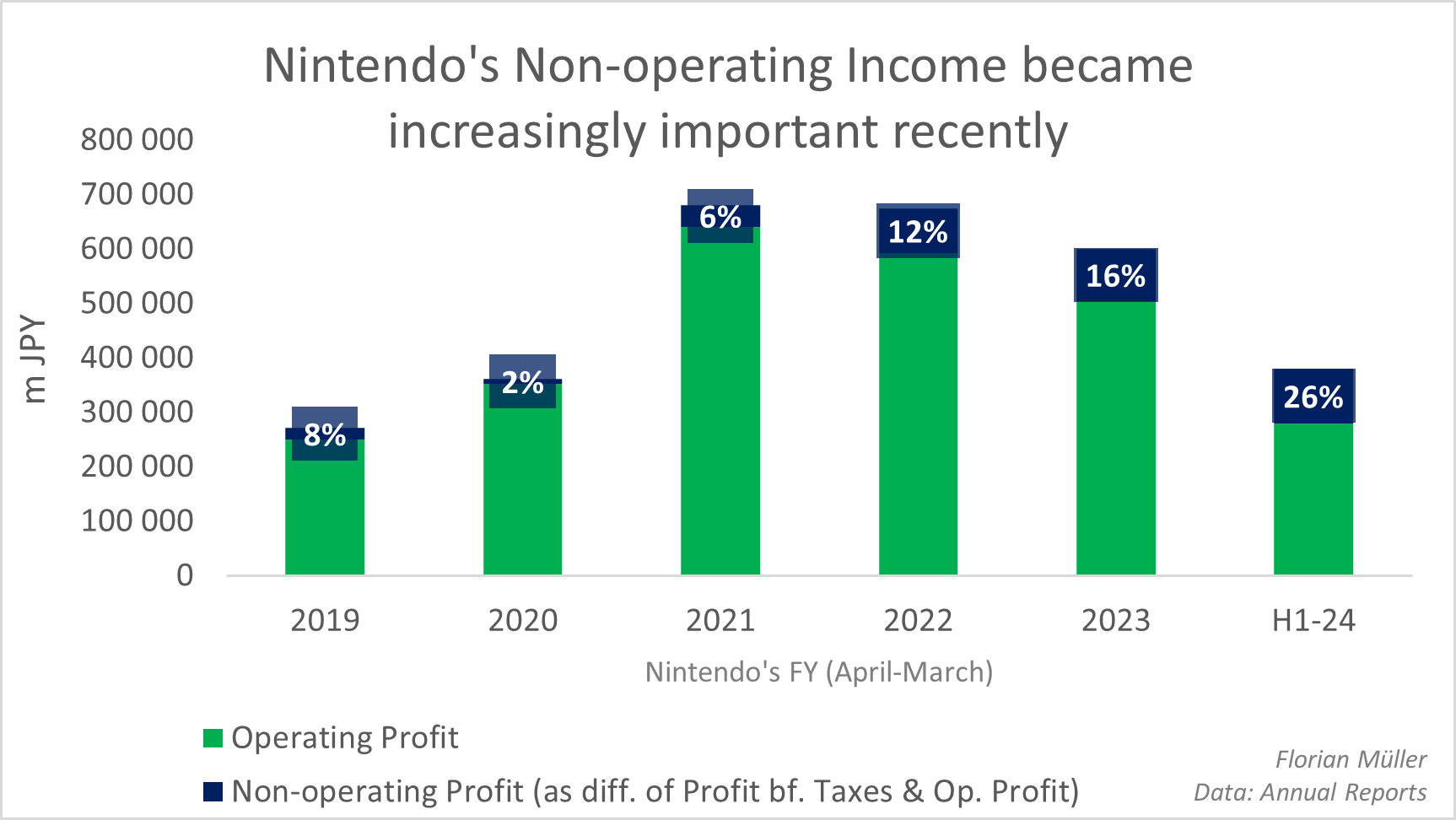

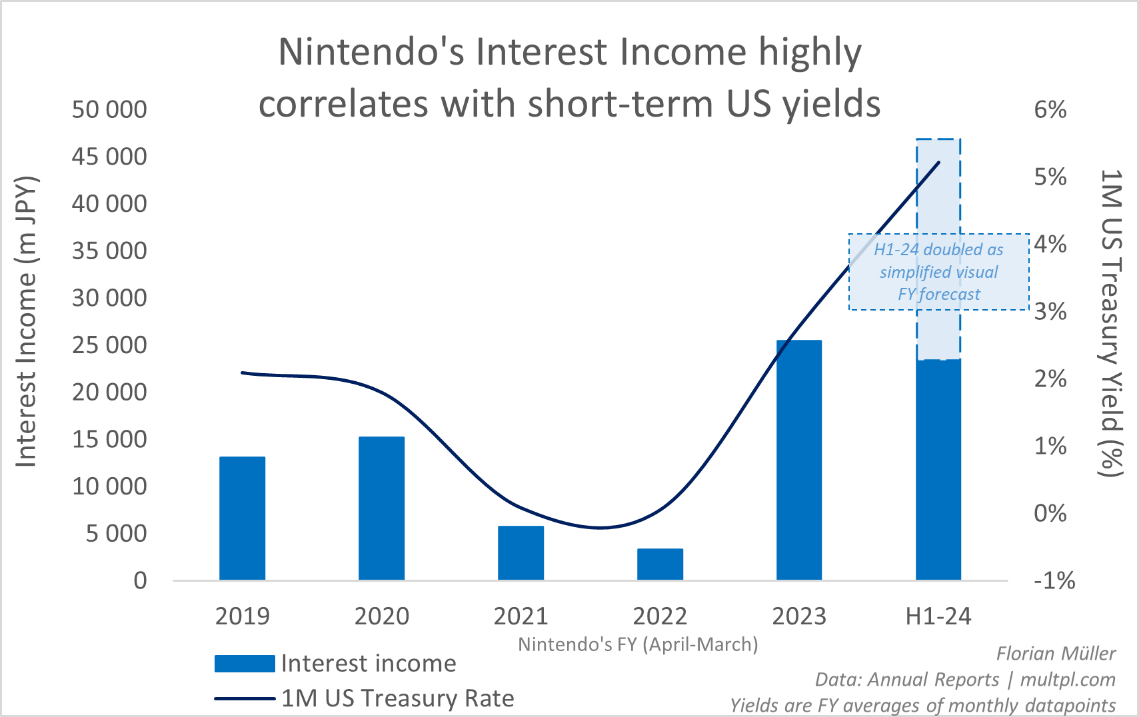

But already now, it is evident how Nintendo’s management strategically leverages its cash surpluses to generate value, recognizable by the growing non-operating income mainly fueled by foreign exchange gains, as previously showcased, coupled with interest earnings.

Florian Müller | Data: Annual Reports

Nintendo’s recent notable increase in interest income from its substantial cash reserves strongly correlates, for instance, with short-term US capital market yields. Thus, Nintendo has been able to significantly benefit non-operationally from the increased interest rate environment abroad, leveraging its high cash holdings.

Florian Müller | Data: Annual Reports, multpl.com

Understating its Product Excellence

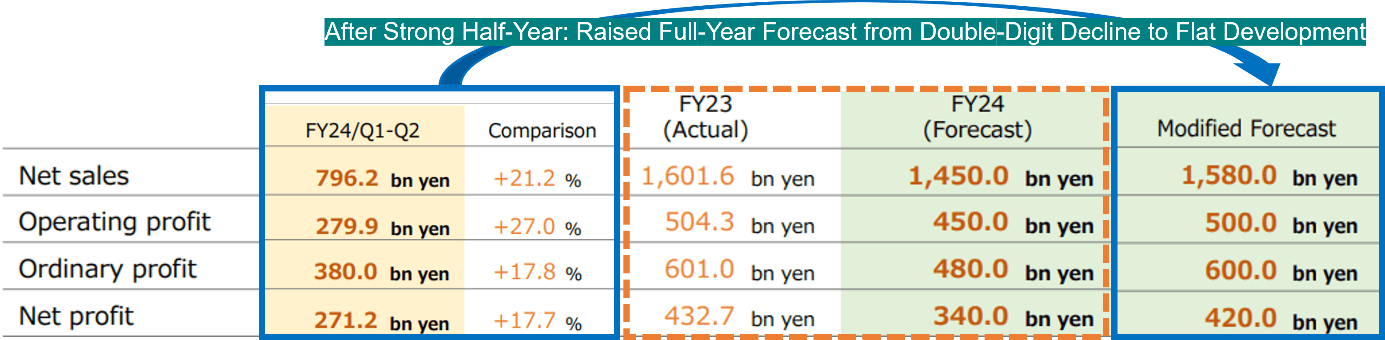

At the end of the first quarter of 2024, which concluded in June, Nintendo reported incredibly robust growth figures, with revenue and profit surging by 50 to over 80 percent compared to the previous year’s quarter. Nonetheless, the management was at first maintaining its annual forecasts, which anticipated a decline of nearly 10 percent in revenue and over 20 percent in earnings. These forecasts could only be an expression of understatement, especially since the first quarter alone has already achieved 30 to 50 percent of these goals. Supported by the recent release of Super Mario Bros. Wonder, whose reviews are overwhelming in various gamer and casual gaming forums, I would not have anticipated a significant decline, substantial enough to not surpass the modest annual targets. Unsurprisingly, the management has now finally revised the forecasts upwards with the latest quarterly results.

Adapted from Nintendo Q2/2024 Earnings Presentation

However, this new forecast still implies a weaker second half of the year. Given its numerically and qualitatively robust pipeline and the holiday season ahead, it’s hard to truly believe in the slowdown projected by the management for the remainder of the year. Instead, this forecast seems once again conservative. The dividend, however, originally estimated to drop by 20 percent to 147 Yen, will instead remain almost flat at 181 JPY for the full year. The interim dividend has already been paid.

Nintendo Q2/2024 Earnings Presentation

Analyst estimates had consistently remained slightly higher in the median when compared to the management’s estimates and still exceed the modified forecast today. This could be because analysts might be considering the ripple effects of the Super Mario Bros. Movie, contrary to Nintendo’s indication earlier this year, that they themselves don’t factor those effects into their financial forecasts.

But even the flat development over the current fiscal year would be particularly pleasing, given that its blockbuster console Nintendo Switch is already in its seventh year since release, with many eagerly anticipating its successor. Up until the fiscal year 2021, console sales had seen significant growth, also fueled by the COVID-induced gaming surge. Nintendo’s product excellence is confirmed by the steadily increasing number of dedicated gamers far beyond 100 million people up until today, even as console sales noticeably declined recently on a fiscal year basis. Management remains reserved about announcing a Next-Gen console. Their primary focus remains on nurturing and expanding the Switch universe. However, ongoing efforts for future hardware are underway. Linked to that might be a hopeful increase in annual research and development spending from 102 billion yen in FY 2022 to a forecasted 130 billion yen in FY 2024.

Value Creation Through Intellectual Property

Nintendo might be gradually reducing its reliance on hardware sales, while the strength of its intellectual property and the popularity of its franchises come to the forefront. Segments involving intellectual property, which include revenue from the film, playing cards, and merchandise, contribute less than 7.5% to the company’s total revenue. Nevertheless, compared to the previous year’s half, these segments have more than doubled, indicating their significant potential as long-term growth drivers. Looking forward, Nintendo has announced to be working on a live-action film of The Legend of Zelda, another one of Nintendo’s highly popular franchises besides Super Mario.

“We do not intend to simply set a numerical sales target for our mobile and IP related business and then aim for that. The use of Nintendo IP requires extremely careful supervision so we don’t negatively affect the image people have of our IP or harm the emotional attachment they’ve formed with it from playing our games. While we always strive to achieve the maximum results possible in each initiative, we do not believe that setting numerical targets such as revenue for the IP related business is appropriate.”

“The Super Mario Bros. Movie,” released since April, has shattered records with almost $1.4 billion in box office earnings, making it the most successful video game film ever. Surpassing hits like “Minions,” it’s tracking to rival major animations like Disney’s “Frozen” and has even outperformed blockbuster franchises like Jurassic Park. Despite mixed critical reviews, the film’s massive popularity reflects the enduring allure of the Nintendo franchise. By strategically showcasing Nintendo in cinemas, the management aims to engage new fans and rekindle interest among former enthusiasts. The film’s positive impact on the “Mobile and Intellectual Property (IP)” segment is boosting this fiscal year’s performance.

Nintendo’s expansion into the analog world includes two Super Nintendo Worlds, reminiscent of Disneyland. The first debuted in Universal Studios Japan, Osaka, in early 2021, followed by another in Universal Studios Hollywood in February 2023. These ventures, inspired by Disney’s theme park success, hint at promising non-gaming avenues for Nintendo’s long-term business. Nintendo doesn’t operate these theme parks themselves because they lack the expertise for it. Instead, they collect licensing fees for them.

Nintendo’s Valuation & Cash Strongly Validate its Share Price

After having discussed the qualitative aspects that make Nintendo an appealing investment despite expected contraction, I aim to quantify this through a conventional company valuation, calculating Nintendo’s fair value.

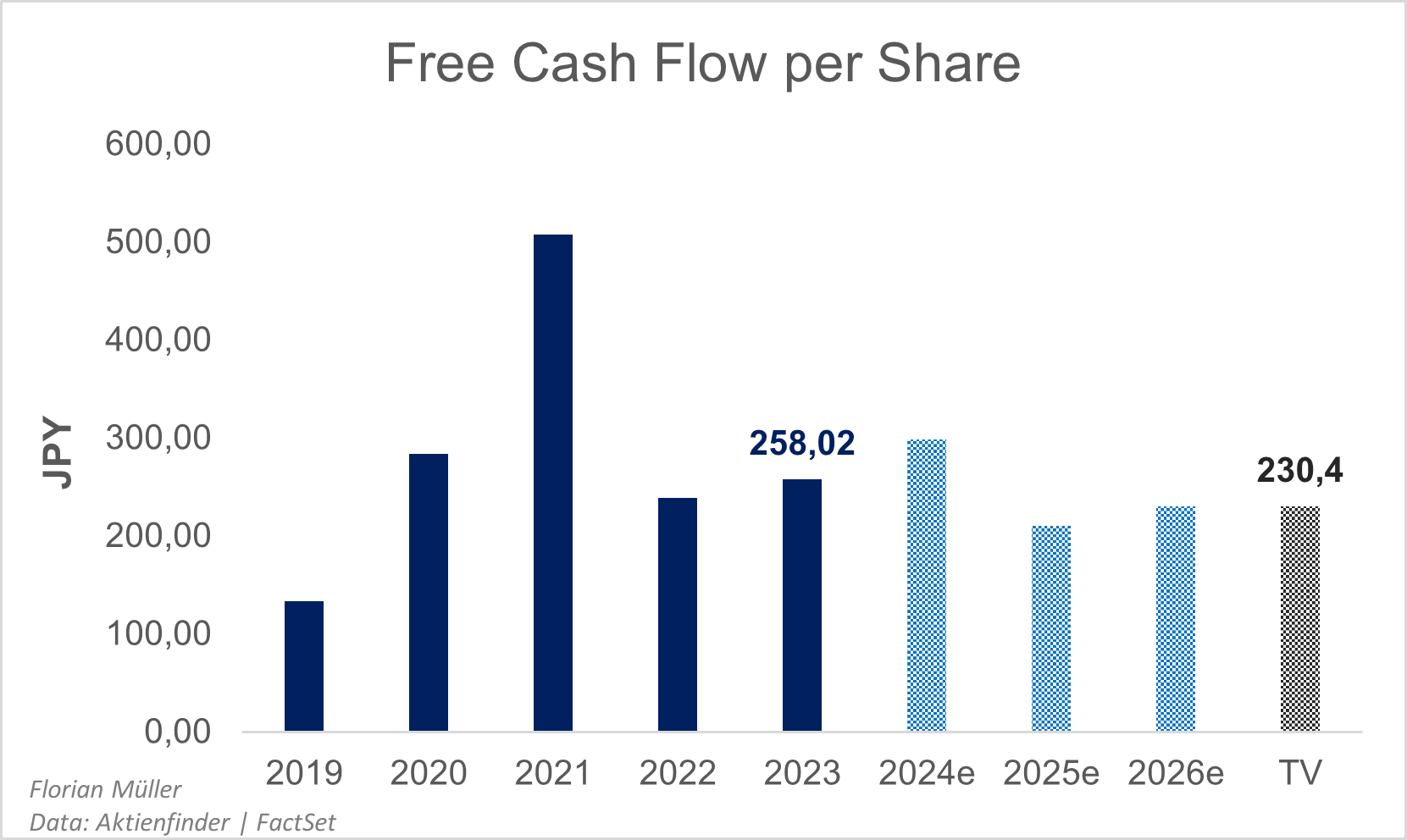

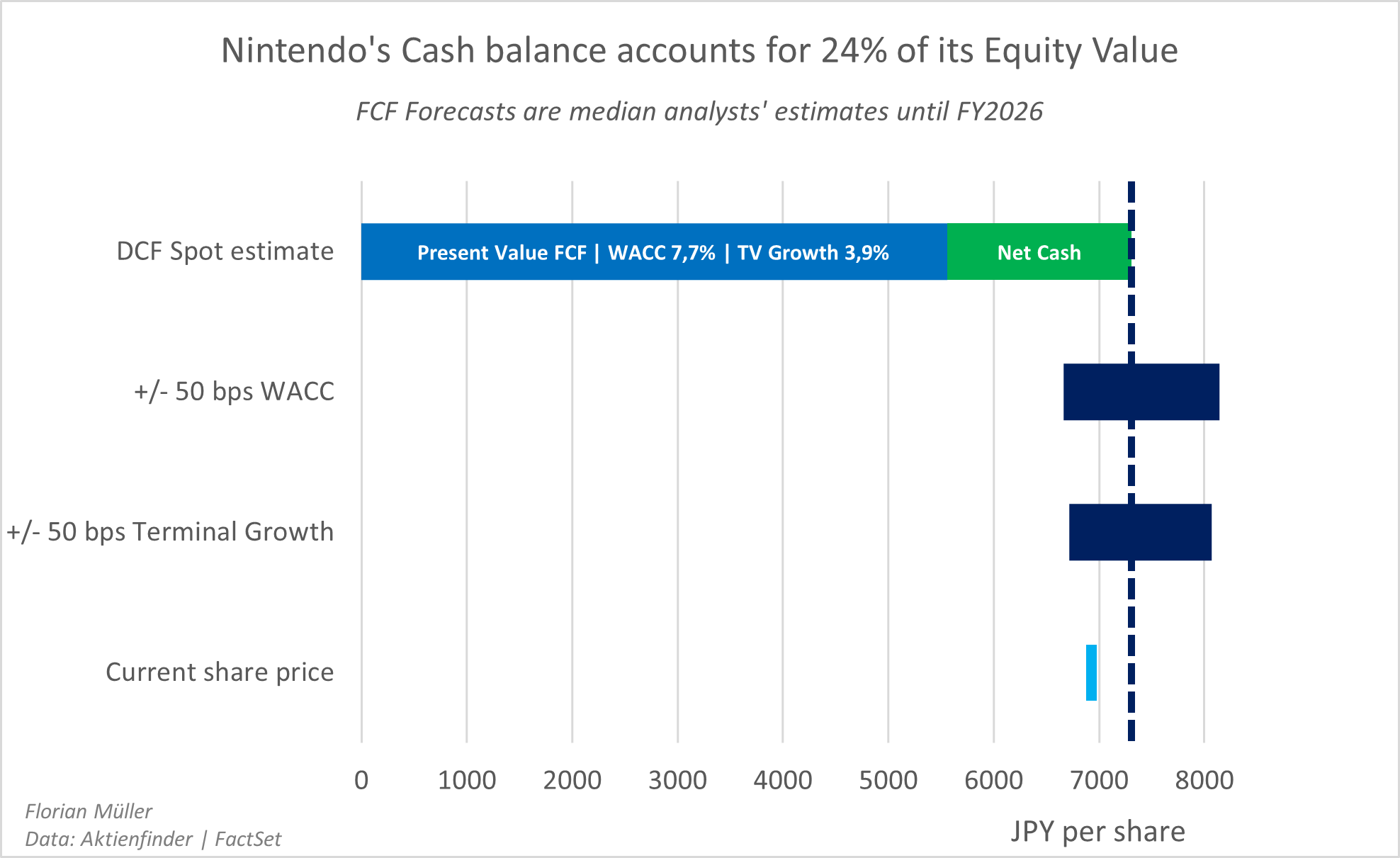

To derive Nintendo’s fair value through a simplified Discounted Cash Flow model, I utilize Free Cash Flow projections sourced from Aktienfinder.net, drawing on median analyst estimates until the fiscal year’s end in 2026, based on FactSet’s database. I successfully cross-verified the actual figures from the last five years for this metric (Free Cash Flow) with those from Seeking Alpha. The Free Cash Flow has stabilized at a conservative level compared to the recent Nintendo Switch boom but remains comfortably high when viewed from a historical perspective. Therefore, I’m using the Free Cash Flow of 2026 as the Free Cash Flow for the Terminal Value.

Florian Müller | Data: Aktienfinder.net, FactSet

My research on Nintendo’s WACC (Weighted Average Cost of Capital) settles at a value of 7.7%. This figure reflects the increased alternative investment opportunities in the risk-free domain due to globally rising bond yields and is supported by Equity Risk Premia per country as published by the renowned Prof. Damodaran. Considering Nintendo’s revenue distribution primarily in mature markets, there are no significant country risks on top of the Equity Risk Premium. Statistically, Nintendo’s slightly lower-than-market-average volatility – expressed in its Beta factor – contributes to keeping Nintendo’s WACC from being excessively high. I derived Nintendo’s Beta factor from a 10-year monthly regression against the Nikkei 225, adjusted using the Blume method. This calculation yielded a Beta factor of around 0.8 to 0.9. Debt financing costs are negligible due to Nintendo’s low level of debt.

I am applying a terminal growth rate of 3.9% into perpetuity, based on the convergence assumption. Within this assumption, I presume that newly invested capital yields neither more nor less than its required cost of capital of 7.7%. Furthermore, I assume that 50% of Nintendo’s Free Cash Flow is reinvested, aligning with Nintendo’s recent 50% dividend payouts and the absence of significant debt obligations.

Florian Müller | Data: Aktienfinder.net, FactSet

Using these parameters, I’ve calculated the present value of Free Cash Flows for Nintendo at approximately 5,560 JPY per share (equivalent to 38 USD at current rates). However, what’s crucial here is Nintendo’s substantial cash reserves, totaling an additional almost 1,745 JPY per share, net of a negligible amount of debt. When factoring in net cash, the total equity value reaches 7,305 JPY per share (equivalent to 50 USD at current rates), slightly surpassing the current share price of approximately 6,900 JPY. While this valuation hinges on my assumptions, it’s evident that Nintendo’s surplus cash significantly bolsters its enterprise value, contributing over 30% on top of it and thus representing a quarter of its equity value.

Weak Spots of This Thesis

Nintendo’s current strengths in benefiting from a weak yen and high interest rates might face risks if these conditions reverse, affecting their non-operating income and the value of their cash reserves. Furthermore, the company’s reliance on the popularity of its franchises is a cornerstone of its success. However, overexploiting these IPs could risk diluting their value over time. The absence of a clear roadmap for a new console, and its potential success, poses a general risk given the ongoing dominance of the existing platform as the primary revenue driver. Any uncertainty surrounding the future console strategy may impact market confidence and Nintendo’s growth trajectory. Investors should consider this alongside the company’s dependence on established IPs when assessing its long-term prospects.

Concluding Insights: Nintendo’s Enduring Value

In essence, Nintendo’s adept handling of currency risks, leveraging of cash reserves, and effective use of intellectual property hint at its resilience and growth potential. Despite near-term projections, the company’s adaptability, innovation, and strong financial foundation suggest promising prospects. The Discounted Cash Flow valuation indicates Nintendo’s surplus cash significantly bolsters its value, offering stability amidst market fluctuations. While short-term concerns exist, encompassing the advanced life cycle of the Switch console without an announced successor model, a potentially devaluing cash basis in declining interest rate scenarios, and currency fluctuations, Nintendo’s management of the latter and its strategic initiatives make it a compelling long-term investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.